Giving financial gifts at Christmas could be a wonderful way to support your children and grandchildren when they need it the most.

Whether you’re keen to help a child buy their first home or provide support with your grandchildren’s school fees, sharing your wealth might bring you and your loved ones great joy this festive season and beyond.

What’s more, the recent Autumn Budget might have nudged financial gifts to the top of your list this year. In her speech, the chancellor extended the freeze on the Inheritance Tax (IHT) thresholds until 2030, and also announced that pensions would be included in a person’s estate for IHT purposes from 6 April 2027.

This could mean that more families will be drawn into the scope of IHT in the coming years, making gifting while living an increasingly attractive option.

So, if you’re thinking about giving financial gifts this Christmas, read on to find out more about IHT and learn how to pass on your wealth as tax-efficiently as possible.

Your loved ones may need to pay Inheritance Tax if your estate exceeds certain thresholds

In the 2024/25 tax year, the standard IHT rate is 40%. This is charged on the amount of your estate that exceeds the nil-rate tax band, which is currently £325,000 (2024/25).

You also have a residential nil-rate band, which is £175,000 (2024/25) and can increase your IHT-free threshold to up to £500,000 if you leave your home to your children or grandchildren.

You can also pass your entire estate to your spouse or civil partner IHT-free, and they can inherit your unused nil-rate bands. So, if you’re married or in a civil partnership, together you could pass on up to £1 million without your loved ones facing an IHT bill.

As mentioned above, these thresholds have been frozen until 2030.

Using your annual gifting allowances and exemptions could reduce a potential Inheritance Tax bill

Each tax year, you are entitled to various gifting exemptions and allowances that you could use to pass on your wealth without your beneficiaries incurring an IHT charge.

Doing so can also reduce the size of your taxable estate, and your IHT liability in turn.

Here are some of the allowances and exemptions you could use to gift wealth this Christmas.

Annual exemption

Each tax year, you can gift up to £3,000 to anybody you like, and the gift will be considered outside of your estate for IHT purposes.

You can also “carry forward” any unused exemption for one tax year. So, if you did not use your gifting exemption in 2023/24, you could gift up to £6,000 in 2024/25.

This could allow you to give a generous gift to your children or grandchildren this Christmas, without worrying about the IHT implications. Remember, if you’re in a couple, you can combine your annual exemptions, allowing you to gift up to £6,000 in a single tax year (or up to £12,000 if you both carry forward your exemptions from the previous year).

Small gift allowance

You can give as many “small gifts” of up to £250 as you’d like each tax year.

However, it’s important to note that this doesn’t apply if you have used another allowance – for example, your annual exemption – on the same person.

Gifts for weddings or civil partnerships

If someone you know is planning to get married or form a civil partnership in the new year, you could give them an IHT-free gift of up to:

- £5,000 to your child

- £2,500 to your grandchild or great-grandchild

- £1,000 to any other person.

You can combine this gift with any other allowance, except the small gift allowance.

This underused exemption could potentially allow you to gift unlimited sums without incurring Inheritance Tax

The “gifts out of surplus income” exemption allows you to gift money from your income directly rather than from your savings.

As there is theoretically no limit to the amount you could gift in this way, gifting from income could be a valuable tax-planning tool.

Yet it is a surprisingly underused exemption. According to the Express, only 430 families used gifting from income in the 2021/22 tax year.

While this exemption is not suitable for making one-off gifts, it’s worth considering if you’d like to give a “gift that keeps on giving” this Christmas.

However, you must meet the key criteria to make use of this exemption:

- Payments should be made regularly, rather than as a one-off event.

- You must be able to meet your usual living costs while making the payments.

- Your gifts must be made from your income, rather than from capital assets.

Read more: Only 430 people used this valuable Inheritance Tax exemption this year – did you?

Giving financial gifts earlier in your retirement might allow you to pass on more of your wealth

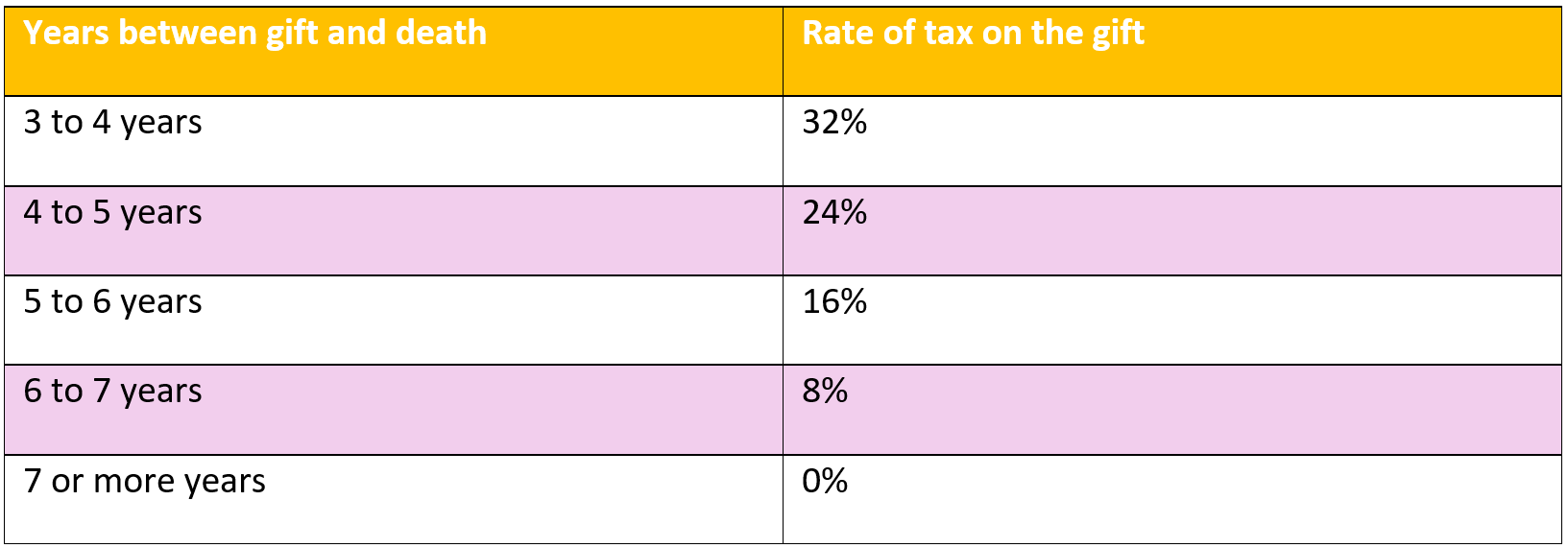

Beyond the exemptions described above, most other financial gifts you make will be treated as potentially exempt transfers (PETs).

The “seven-year rule” applies to PETs, which means that they will only be free from IHT if you survive for at least seven years after making the gift.

If you die before this, your gift may be subject to IHT if it exceeds your nil-rate band.

The amount payable depends on how long you live after making the gift. The table below shows how this “taper relief” works.

Source: gov.uk

As you can see, giving a festive financial gift to your children or grandchildren earlier in your retirement could allow you to pass on more of your wealth. You’ll also be able to enjoy seeing them benefit from their inheritance.

We can help you plan how to give financial gifts tax-efficiently

If you’re considering giving financial gifts for Christmas this year, our financial planners can ensure that you make the most of gifting allowances and exemptions to reduce a potential IHT bill.

Importantly, we can also help you understand how much money you can afford to gift without compromising your long-term financial plan.

It may be that there are alternatives to direct gifting that might suit your needs, such as setting up a trust for your children and grandchildren.

Together, we can explore your options and create a plan that meets your specific goals and preferences.

Get in touch

If you’re considering giving financial gifts over the festive season, we can help you pass on your wealth as tax-efficiently as possible.

To find out more, please get in touch. Email hello@sovereign-ifa.co.uk or call us on 01454 416653.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning or tax planning.

Remember that taper relief only applies to gifts in excess of the nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief.

Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.

Approved by Best Practice IFA Group 17/12/2024.