With the current state of the UK economy, high inflation, and rising interest rates, it’s important to know how to protect and grow your wealth effectively.

However, a new survey by Aviva has revealed that more than half of UK adults don’t understand how high inflation affects their cash savings.

Read on to find out what rising interest rates and high inflation mean for your money and what you can do to help protect your financial future.

How inflation has changed in recent years

Latest figures from the Office for National Statistics (ONS) show that, as of March 2023, the UK’s inflation rate stood at 10.1%. Back in March 2021, the rate was just 0.7%.

There are several factors that have led to the inflation rate rising since March 2021. One of the biggest causes has been the soaring cost of energy. Already in greater demand as life slowly got back to normal after Covid, oil and gas reserves were put under further pressure by Russia’s invasion of Ukraine.

Alongside that, the war in Ukraine also reduced the amount of grain available, increasing demand and pushing up food prices across the globe as a result.

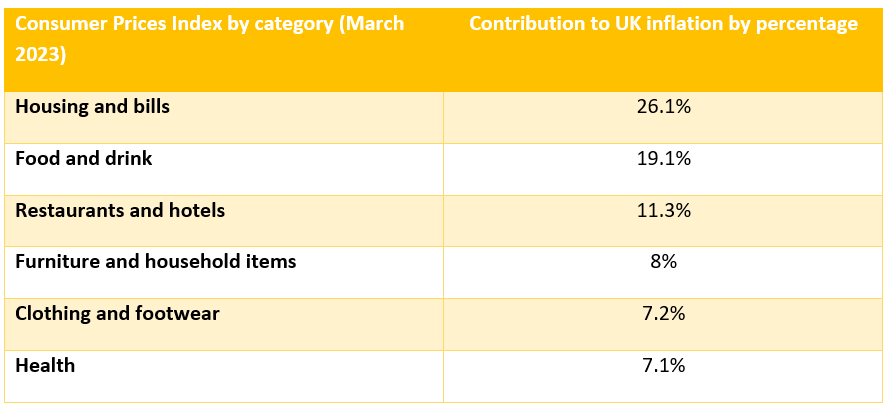

The table below shows how different goods and services have contributed to UK inflation, with housing and utility bills being the biggest contributor, as of March 2023.

Source: ONS

To try and slow inflation rises, the Bank of England (BoE) has increased interest rates 11 times between December 2021 and April 2023.

While this may be good news for savers, it also makes borrowing more expensive, meaning mortgage rates have also increased. When people have less money to spend, they typically purchase fewer items – the theory being that this can reduce the demand for goods and, as a result, slow price rises.

Remember that even if the inflation rate does reduce, prices won’t fall; they just won’t rise as quickly.

Your cash savings are likely worth less in real terms than a year ago

When thinking about savings and investments, it’s important to fully understand how the inflation rate will make a big difference to whether your wealth grows in real terms.

The inflation rate means that goods and services are generally more expensive than they were a year ago. The current inflation rate (as of March 2023) of 10.1% means that goods and services that cost £100 a year ago cost £110.10 now.

According to Moneyfacts, as of 5 May 2023, the best instant access savings account pays an interest rate of 3.71%. So, if you’d saved £100 into that a year ago, you’d have £103.71 now.

You can see that the value of your cash savings has not kept pace with rising prices, meaning your cash is worth less in real terms.

Research by pension provider Royal London goes one step further to show the effects of inflation on £10,000 in savings.

The research reveals that a sustained inflation rate of 5% over 10 years could reduce your money’s value by 34% in real terms, bringing its spending power down to just £6,564.

How you can protect your savings

If you’re currently considering your options and how best to protect yourself and your savings from inflation, one option you might consider is investing.

As investing is typically a strategy if your time frame is five years or more, it can be an ideal option if you are looking to save or invest in the medium to long term.

Research carried out by Vanguard Investor highlights the fact that the stock market traditionally performs well compared to cash savings.

Comparing data between 31 December 1900 and 31 December 2022, cash generated an average real annual return of 0.87% and UK shares saw an average real annual return of 5.35%.

Adjusted for inflation, the £10,000 invested in UK shares in 1900 would have been worth £75,270 in 2022, giving a real return of £65,270. This is assuming that dividends and income were reinvested.

Comparatively, the same amount invested in cash would have been worth around £20,614.

Whenever considering investing your money or savings, it’s important to remember that investing is typically a long-term venture and previous performance is never an indicator of future success.

The value of stocks and shares can rise and fall at any moment but when you view returns across a long period of time, the usual peaks and troughs historically smooth out.

Remember also that it is often prudent to retain some funds in cash. For example, it is usually advisable to have an emergency fund of between three- and six-months’ expenses in an easy access account that you can dip into if you need to.

Get in touch

If you want to know the best way for you to protect your savings and financial future, speak to us. We’ll work alongside you to create a long-term financial strategy that can help you to achieve your goals. Email hello@sovereign-ifa.co.uk or call us on 01454 416653.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.