On 30 October, chancellor Rachel Reeves delivered the new Labour government’s first Budget.

In the weeks and months before the announcement, Reeves warned of the need to make “difficult decisions” to fill a “£22 billion black hole” in the nation’s finances. So, significant tax changes were expected.

Indeed, there was widespread speculation that Capital Gains Tax (CGT) rates would be brought in line with Income Tax rates. According to the Guardian, this could have raised up to £14 billion, which would have given a significant boost to the public purse.

While the chancellor did not go quite this far, she did introduce several CGT reforms that you may need to know about.

Read on to learn more about changes to CGT announced in the Budget and find out three useful ways to adapt your financial plan and mitigate any potential negative effects.

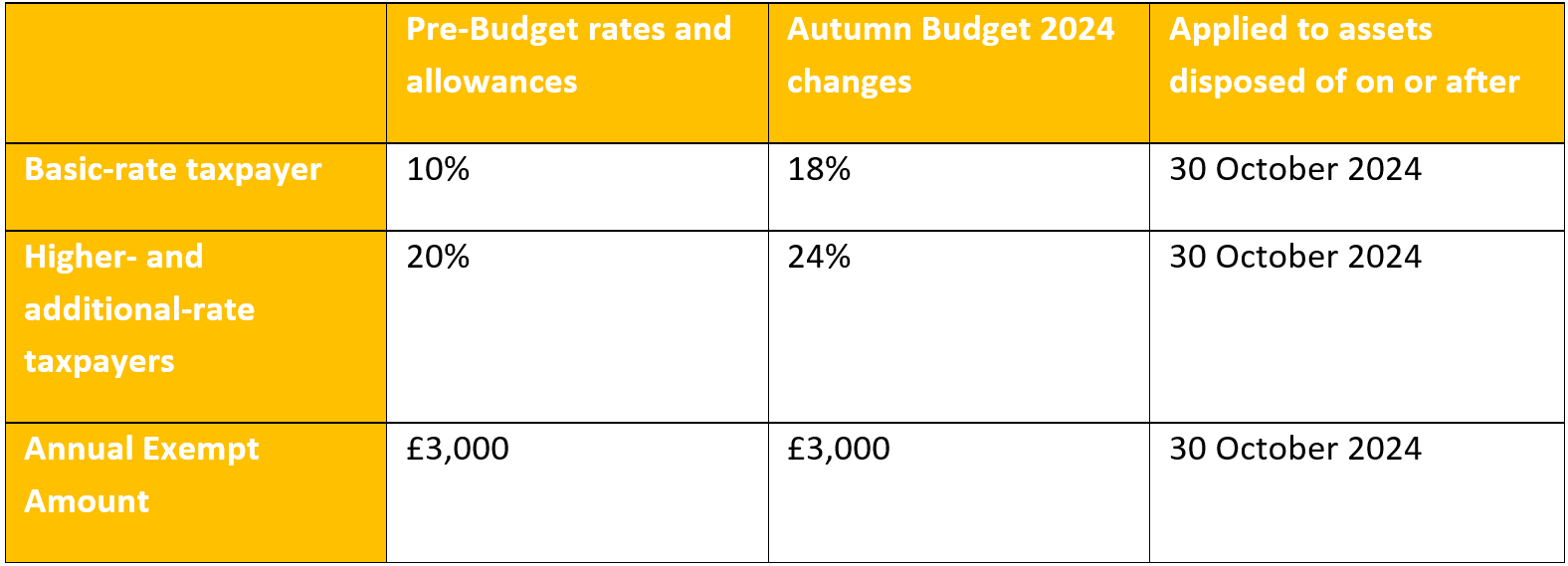

The Annual Exempt Amount remains unchanged, but Capital Gains Tax rates have increased

One option the chancellor might have pursued to raise much-needed public funds was to lower the CGT-free allowance.

You can usually make gains of up to £3,000 (2024/25) in a single tax year without incurring CGT. This is your “Annual Exempt Amount”.

The previous government had already reduced the CGT allowance from £12,300 in the 2022/23 tax year, to £6,000 in 2023/24, and again to £3,000 for 2024/25.

So, it came as welcome news in the Budget that the Annual Exempt Amount remains at its current level.

However, Rachel Reeves confirmed an increase in the rate of CGT, which took effect immediately (from 30 October 2024). These rates apply to most chargeable assets and there are no longer separate rates for residential property disposals. The rate of CGT you pay falls in line with your marginal rate of Income Tax.

The table below shows the new rates and allowances in comparison to the pre-Budget figures.

Source: gov.uk

As you can see, these changes could result in a significant increase in your CGT liability.

Imagine that you are a higher-rate taxpayer who sold an asset for a profit of £20,000 before 30 October. You likely would have paid 20% CGT on your taxable gain of £17,000 (£20,000 minus your Annual Exempt Amount of £3,000), equating to £3,400.

Yet, if you made the same gain after the Budget, you would pay 24% CGT, a total of £4,080.

While these increases might not seem appealing, it’s worth remembering that the Budget changes could have been considerably less favourable for those affected by CGT.

Had Rachel Reeves brought CGT rates in line with the higher-rate Income Tax band – an option that was rumoured to be on the table – you could have faced an even bigger increase in CGT, to 40%.

Tax relief for businesses and investors disposing of assets has been reduced

As a business owner or investor, you might rely on Business Asset Disposal Relief (BADR) or Investors’ Relief (IR) to manage your CGT liabilities.

If you’re eligible, BADR allows you to pay less CGT when you sell or “dispose of” all or part of your business.

As an investor, IR could reduce the amount of CGT you pay when disposing of qualifying investments that were issued on or after 17 March 2016 and disposed of on or after 6 April 2019.

Currently, if you’re eligible for BADR or IR, you’ll pay CGT at 10% on all gains on qualifying assets.

However, in the Budget, the chancellor announced that for those who are eligible for BADR or IR, the rate of CGT will rise to 14% from April 2025, and to 18% from April 2026.

So, if you’re considering selling your business, shares in a business, or investments, and you were banking on making the most of these types of relief, the clock is ticking. After April 2025, when the new rates take effect, you could incur a considerably higher CGT bill.

Additionally, the lifetime limit for IR has been reduced from £10 million to £1 million – effective from 30 October 2024. As a result, if you benefit from IR and have lifetime gains above £1 million, the standard rates of CGT will apply to the excess.

It’s also worth noting that the reduced CGT rates for carried interest – paid by private equity managers – will rise from 18% and 28% to 32% from 6 April 2025, with plans for further reforms from April 2026.

3 useful ways to reduce your Capital Gains Tax bill

While the CGT changes introduced by the Budget might seem off-putting, we can help you manage them effectively as part of your long-term financial plan.

Here are three strategies for reducing your CGT liability.

1. Make full use of tax-efficient wrappers

The new CGT rates make tax-efficient wrappers, such as ISAs and pensions, even more valuable.

Any gains you make on investments held in an ISA are exempt from CGT (there’s also no Income Tax or Dividend Tax to pay on the interest and dividends you receive).

The Budget confirmed that annual subscription limits for ISAs will remain at current levels until 5 April 2030. This means that you can add up to £20,000 to your ISAs in a single tax year.

If you’re a higher- or additional-rate taxpayer, investing within ISAs may be especially attractive, as it could allow you to protect some of your wealth from the new 24% CGT rate.

What’s more, if you have a spouse or civil partner, you could combine your ISA allowances and save up to £40,000 tax-efficiently.

You could also add up to £9,000 each tax year into a Junior ISA (JISA) for your child – this won’t affect your adult ISA allowance and provides further tax-efficient investing opportunities that benefit the next generation.

Pensions are another powerful tax-efficient wrapper. You could receive between 20% and 45% tax relief, depending on your income. So, it might also be worth increasing your pension contributions.

2. Transfer assets to your spouse or civil partner

Following the Budget, the spousal exemption remains in place. This means that usually, you won’t pay CGT on assets you give or sell to your spouse or civil partner.

So, you could reduce the amount of CGT you’ll pay as a couple by taking full advantage of your individual allowances.

For example, if you use up your own Annual Exempt Amount in any given tax year, you could transfer any CGT-liable assets into your partner’s name before disposing of them, to make the most of any remaining allowance they have. Remember: the Annual Exempt Amount is a “use it or lose it” allowance that can’t be brought forward if unused in a previous tax year.

Alternatively, an inter-spousal transfer could help to reduce your CGT bill if your spouse or partner pays a lower rate of Income Tax than you.

3. Reduce your taxable income

As the rate of CGT you pay depends on your Income Tax band, lessening your taxable income could reduce your CGT liabilities.

If you’re still working, a useful way to do this is to increase your pension contributions to bring yourself into a lower Income Tax band, perhaps using a salary sacrifice scheme.

This could not only reduce your CGT liability in the short term but also increase the value of your retirement savings in the long term.

However, you may pay Income Tax when you withdraw from your pension. Being strategic about how you draw your pension wealth when the time comes could help you avoid unnecessary Income Tax.

And, if you’re already retired, you might be able to reduce the amount of income you take flexibly from your pensions by drawing on other sources, such as ISAs, which don’t attract Income Tax. This could help you to stay in a lower tax bracket and avoid the highest rates of CGT.

Overall, choosing to carefully draw funds from several sources – some of which attract Income Tax and CGT – could prevent you from exceeding certain tax brackets and help you keep more of your wealth.

Get in touch

If you’re concerned about how to navigate the Budget changes to CGT rules, we can help.

To find out more, please get in touch. Email hello@sovereign-ifa.co.uk or call us on 01454 416653.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Approved by Best Practice IFA Group 19/11/2024