Pensions are an exceptionally tax-efficient way to save for retirement.

Generous tax relief on contributions means that a £100 contribution only “costs” a higher-rate taxpayer £60. When you add in positive investment returns and, potentially, employer contributions it’s easy to build up a substantial fund quickly.

Of course, there’s a catch. The Lifetime Allowance (LTA) imposes a limit the amount of tax-efficient savings an individual can accrue across their lifetime, with tax charges typically falling due if a client exceeds this limit.

In 2021, the chancellor froze the LTA at £1,073,100 until at least 2026.

It’s easy for your clients to think that having a pension pot worth £1 million is simply something that will never happen to them.

However, new figures reported in Money Marketing show there has been a steep increase in the number of people affected by the LTA.

Strong investment returns and a freeze in the threshold mean almost 30,000 people are likely to be caught by the LTA by 2026, leading to tax charges of an eyewatering £1.5 billion.

Read on to find out more about how the LTA could affect more clients than you think.

The LTA has been falling – here’s how to calculate a potential liability

The LTA was introduced in the tax year 2006/2007 and represents the total amount an individual can build up in pension benefits without incurring a tax charge.

At the time of its introduction, the LTA was fixed at £1.5 million. Having reached a peak of £1.8 million in 2011/12, it has gradually reduced since and now stands at just over £1 million.

If clients exceed the LTA, they are liable for a 25% tax charge on any amount above the allowance taken as income, and 55% on any amount drawn as a lump sum.

- If a client has a defined contribution pension, then calculating the LTA is quite easy – it is simply the pension investment fund value.

- If it’s a defined benefit scheme, the equivalent fund size is the annual pension payable multiplied by 20, plus any lump sum that is payable in addition. Pensions taken before April 2006 are valued by multiplying the pension payable by 25.

If a client has a mixture of pension types, they need to be added together to work out their LTA position.

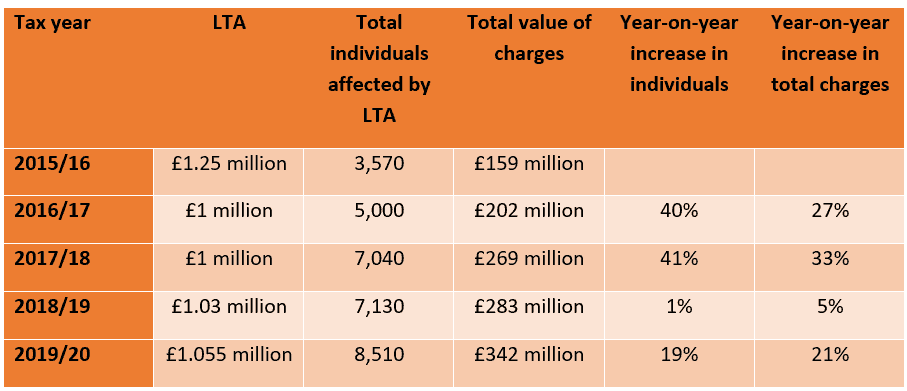

The number of people facing LTA charges is growing sharply

In 2019/20, LTA tax charges affected 8,510 people, raising £342 million in tax.

Source: Money Marketing

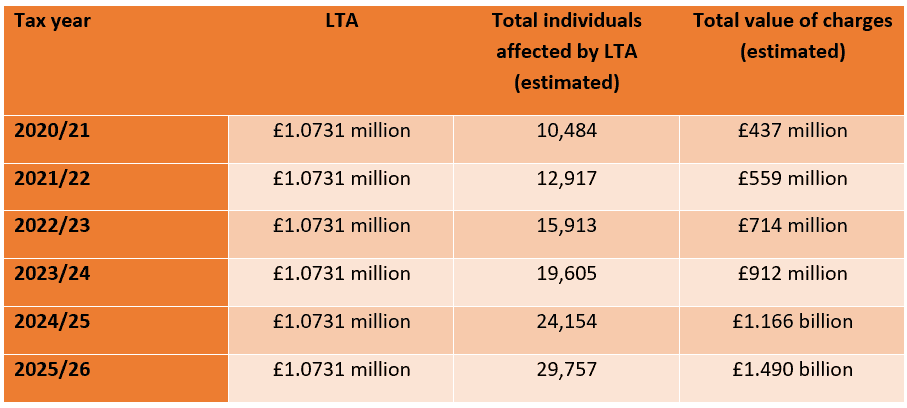

Now, analysis from insurer Canada Life shows that the numbers of people likely to be affected by the LTA is set to rise sharply in the coming years.

Canada Life technical director, Andrew Tully, says: “Over the last five years, it [the value of charges] has gone up on average by 28% a year. If we assume it keeps growing up the same rate, in a few years’ time, we will get to about £1.5 billion.”

The insurer has estimated how many people will be affected by the LTA, and the total tax take, until the 2025/26 tax year.

Source: Money Marketing

These forecasts show that the number of people caught by the LTA is predicted to hit 29,757 and raise nearly £1.5 billion in tax by 2026.

The LTA is likely to affect more and more of your clients

While a £1 million pension pot might seem like a long way away for many clients, someone looking to retire on a modest income for 30 years or more could easily need that amount in their fund.

Additionally, it’s worth remembering that someone with £600,000 in their pension now will exceed the current LTA in 15 years’ time even just assuming 4% annual growth.

As, historically, pension funds and salaries have grown faster than inflation it is likely that more and more clients will be affected by the issue in the future.

It’s also worth reminding clients that LTA issues can often arise on divorce. Where there are significant pension assets, sharing pensions can see one or both parties end up with a pension that is valued above the LTA.

Financial planning can help your clients tackle LTA issues

If you have clients who may face LTA issues in the coming years, working with a financial planner can add value.

For example, we can look at a range of strategies such as:

- Considering other types of tax-efficient saving, such as ISAs

- Applying for “fixed” or “individual protection” – this can protect an individual’s LTA at a higher amount

- Continuing to contribute and paying the 25% tax charge. If a client is benefiting from employer contributions, tax relief, and investment growth it may well be that they are still better off even if they do pay a 25% tax charge.

We can model a client’s future to establish whether they are likely to have LTA issues, and then provide advice on ways to mitigate any potential tax charges.

If you have clients that would benefit from advice, or you’re interested in how you can work more closely with us, please get in touch. Email hello@sovereign-ifa.co.uk or call 01454 416653.