Many people put off estate planning because it involves difficult conversations with loved ones. According to Today’s Wills & Probate, only 15% of parents discuss inheritance with their children.

Unfortunately, failing to put an estate plan in place could lead to financial difficulties and disagreements down the line.

Dying Matters Awareness Week runs from 4 to 10 May, and this year’s theme is “Let’s talk about death and dying”. As such, it’s an ideal time to remind clients about the importance of getting their affairs in order.

Read on to find out how solicitors and financial planners can work together to help clients protect their wishes and provide for loved ones by putting robust estate plans in place.

Maximise the tax efficiency of clients’ estate plans

When deciding how and when to pass on assets to the next generation, there are several taxes your clients may need to consider, including:

- Inheritance Tax (IHT)

- Capital Gains Tax (CGT)

- Income Tax

- Stamp Duty Land Tax (SDLT)

A financial planner can help your clients structure their estate plans for maximum tax efficiency, ensuring their chosen beneficiaries receive as much of their wealth as possible. For example, they may take steps to make the most of available IHT allowances and reliefs or place assets in a trust.

They can also use cashflow modelling to show clients how income from their estate or any trusts they leave will be taxed and how different reliefs might apply in practice. This includes stress-testing against any potential changes to reliefs, so that clients can adapt their estate plan over time to keep it as tax-efficient as possible.

As a solicitor, you can support this process by ensuring that strategies and documents, such as wills, are legally compliant and reflect the individual’s wishes.

Working together in this way could allow clients to pass on more of their wealth and adapt smoothly to tax-law changes.

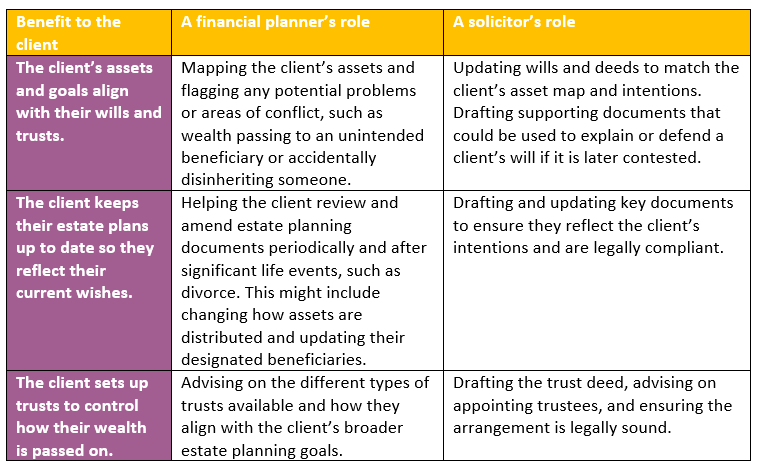

Help ensure clients’ wills are undisputed

Yahoo! recently reported that family inheritance disputes hit their highest levels in more than a decade in 2024; more than 11,300 wills were challenged compared to 10,410 in 2023.

Through joined-up working, financial planners and solicitors can play an important role in reducing the risk of disputes and protecting clients’ wishes. The table below shows how this might work in practice.

By minimising the risk of challenges, financial planners and solicitors can provide clients with invaluable peace of mind that their wishes will be followed and their loved ones will not face the stress of legal disputes.

Navigate upcoming changes to Inheritance Tax

Under current rules, pensions are not generally included in a person’s estate for IHT purposes. As such, they have frequently been used to pass on wealth tax-efficiently.

However, from April 2027, most unused pensions and death benefits will be included in IHT calculations.

This change is likely to mean that many of your clients may benefit from reviewing and potentially amending their estate plans. Indeed, Pensions Age has revealed that more than half of UK adults are planning to adjust their retirement or estate plans in response to the government’s planned changes to IHT rules.

A financial planner can stress-test your clients’ existing plan against the upcoming IHT rule changes and show how different gifting or restructuring strategies might affect their beneficiaries’ financial position. As a solicitor, you can then translate their chosen option into legally robust structures, such as updating mirror wills or creating codicils.

Collaborating in this way could make it easier for clients to understand how the planned IHT reforms might affect them and help them feel prepared for these changes rather than concerned.

Get in touch

If you have clients who need help creating or updating their estate plans to safeguard their wishes and the financial security of loved ones, we can help.

To learn more about how we can work together, please email hello@sovereign-ifa.co.uk or call us on 01454 416653.

Please note

This article is aimed at professional advisers only and does not constitute advice.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning, cashflow planning, tax planning, trusts, or will writing.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Approved by Best Practice IFA Group Ltd on 13/4/26