In the last two years, the Bank of England has increased the base rate 14 times in an attempt to control soaring inflation.

Consequently, interest rates are at levels we haven’t seen since before the global financial crisis. As of 25 November 2023, Moneyfacts reports that it’s possible to secure more than 5%, even on an easy access account.

Higher interest rates have tempted many people into cash and away from investing.

As an example, This is Money reports that National Savings & Investments recently had to pull a guaranteed one-year bond paying 6.2% because of overwhelming demand.

So, does investing even make sense anymore?

The rules of capitalism haven’t changed in 2023

Firstly, it’s important to remember that the laws of capitalism haven’t changed.

Governments need to raise money through debt. The Office for National Statistics (ONS) reports that public sector net borrowing (excluding public sector banks) in October 2023 was £14.9 billion.

Consequently, they have to pay higher returns than cash to borrow.

If cash rates are at 5%, government bonds have to offer you more than that to tempt you out of the bank – even more so if they want you to lock it up for 10 years.

Then, remember that companies have to pay more than governments to borrow.

Companies need to incentivise you to lend to them, rather than to the government – and this means paying you more than the government does!

If cash rates are 5%, and government bonds offer 6% (for example), corporate debt must be higher again. Otherwise, why would you take the risk?

Equities have to offer the chance of being paid more than corporate bonds.

That’s because companies also need to generate money for their shareholders (who are taking even more risk than their bondholders).

If a firm’s shareholders could do better leaving their money in the bank, pretty soon there would be no shareholders – and decision-makers at companies know that.

Any new project requiring a cash investment will be judged against the bank rate. If a new project doesn’t have the potential to beat what the bank’s offering, why do it?

The bottom line is that cash sets the bar. Everything else then needs to jump over it.

“This time it’s different!” – but is it?

Of course, it’s tempting to believe that today’s investment circumstances are unique: “This time it’s different!”.

Inflation remains stubbornly high. Government debt levels have soared (the ONS says net public sector debt is estimated at around 97.8% of the UK’s annual Gross Domestic Product). Geopolitical hotspots are flaring up in Ukraine, the Middle East, and Taiwan.

Then you must consider the transformational developments in AI and the increasingly savage impact of climate change.

But is it really different this time?

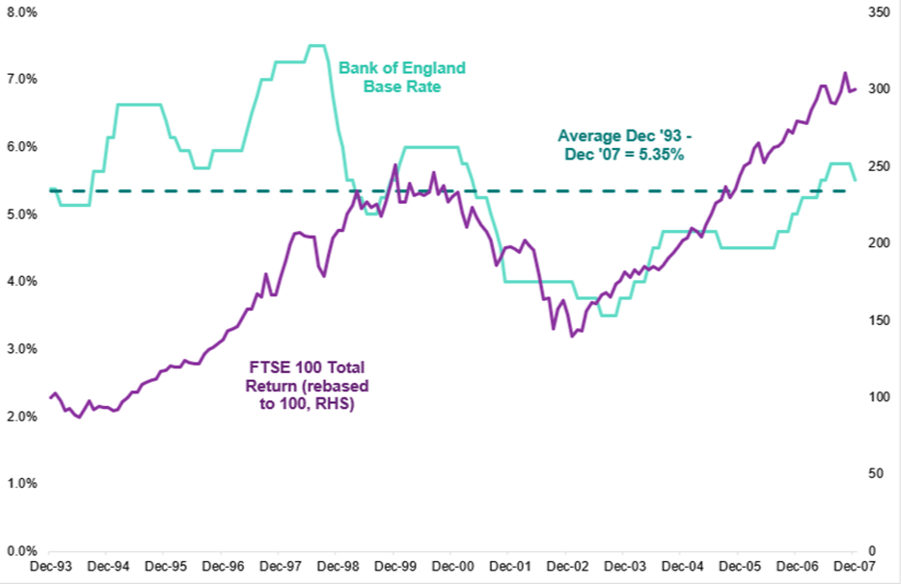

Take a look at the chart below:

- Between 1993 and 2007, interest rates averaged 5.35%.

- Government debt levels were rising sharply (UK government debt went from 20% of GDP in the 90s to more than 50% in the noughties, and lots of people were extremely worried about it)

- Geopolitical hotspots were flaring up in Yugoslavia, the Middle East, and Russia

- The internet was revolutionising society.

In the face of all that, surely just staying in cash, at 5.25%, was best?

Absolutely not.

Source: 7IM/Factset

That higher cash bar created better jumpers. The FTSE 100 (with dividends reinvested) returned 8.1% annualised over that period.

The world continued to jump over the bar, and it will likely do so in the next economic cycle too.

Get in touch

Investing can offer the potential for better long-term returns, which can help you to achieve the growth you need to meet your long-term goals.

To find out more, please get in touch. Email hello@sovereign-ifa.co.uk or call us on 01454 416653.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

The Financial Conduct Authority does not regulate NS&I products.