“The strength of a family, like the strength of an army, lies in its loyalty to each other.”

These are the words of Vito Corleone, the patriarch of the crime family brought to life on screen by the great Marlon Brando.

It’s 50 years since the release of The Godfather – generally regarded as one of the most important films ever made. The winner of three Oscars, the film spawned two sequels and made household names of the likes of Al Pacino, Diane Keaton, and the late James Caan.

The family-owned business we work with don’t run their enterprise in quite the same way as the Corleones operate their mafia empire. However, all of them see great value in working with us, and multigenerational planning can provide great benefits to these clients.

Here are four useful pieces of advice we’d offer to all family-run businesses.

1. Formalise roles as you grow

Most small businesses begin around the kitchen table or in a small premises somewhere. While it’s easy for clients to have discussions and keep things informal when the business is small, as the enterprise grows it’s important to start to formalise the structure.

If clients have multiple family members involved in the business, it can sometimes seem cold to start to put shareholder agreements and other formal structures into place.

However, properly minuted meetings and partnership or shareholder agreements are essential so people know where they stand if they decide to leave, someone unexpectedly passes away, there’s a divorce, or other people want to join.

While some disagreement in business is inevitable, the added danger in family-run businesses is that it can damage relationships and create real resentment that could drive a wedge between various members of a client’s family.

2. Include the whole family in your financial plan

One approach that we find really works for clients is when we advise multiple generations of the same family.

This is an increasingly popular choice among advised clients, with a recent M&G Wealth report revealing that 1 in 3 advised families now share the same financial planner, with around 3 in 5 of those sharing the same adviser as their parents.

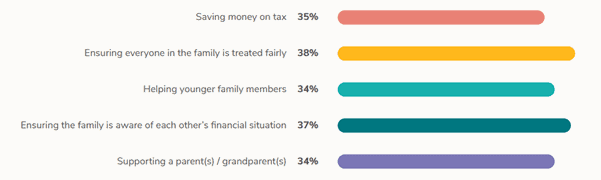

The key benefits of this to clients can be seen below.

Source: M&G Wealth

From ensuring the smooth transfer of wealth between generations to reducing a tax bill (more of this below) there are many reasons an intergenerational financial plan covering two or more generations can add real value to a family and, consequently, their business.

3. Make sure you are tax-efficient

One of the key benefits for clients planning as a family is that it can reduce the amount of tax paid.

For example, if a client loses a parent who bequeaths a business, this could come with a sizeable Inheritance Tax (IHT) bill which could put the viability of the company in jeopardy.

Working with multiple generations can help us to make use of measures such as Business Relief to mitigate some or all of a potential IHT bill.

Read more about Business Relief and estate planning in our blog.

We can also use cashflow modelling to determine whether older generations can make gifts to younger family members now, potentially removing the value of these gifts from their estate for IHT purposes.

Family Investment Companies can also be a tax-efficient vehicle for protecting wealth for future generations.

These structures can help pass wealth and assets to future generations in an appropriate way, and are an increasingly popular choice for successful family business owners as part of their broader succession and tax planning strategy.

4. Remember it’s about the parents and the children

One trap many business owners fall into without advice is that they focus too much on what they can pass onto their children, not on what they can do to help themselves.

While it’s important for clients to help the next generation, it shouldn’t necessarily come at their own expense.

For example, increasing their pension contributions while they are working can help clients become less financially dependent on the business, making it easier for them to hand over control.

Pensions ensures clients accumulate funds for later life in a highly tax-efficient manner, and they can also be a very tax-efficient way to pass on wealth on death.

Creating a family financial plan can ensure that the needs of every individual are met – whatever stage of life they are at.

Get in touch

We work with many family-owned businesses and can help your clients to get the most from their wealth.

If you have clients that would benefit from advice, or you’re interested in how you can work more closely with us, please get in touch. Email hello@sovereign-ifa.co.uk or call 01454 416653.