Any links will direct to a third-party website and Sovereign IFA Ltd is not responsible for the accuracy of the information contained within linked sites.

Over the past few years, inflation (the rate at which the general level of goods and services rises) has barely left the headlines, and it’s been a common concern among business owners in the UK.

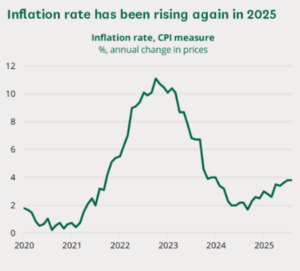

The government’s target is to keep inflation at 2%. However, as you can see in the UK Parliament chart below, inflation has remained above this level for most of the past three years, with the exception of a brief period in mid-2024.

Source: UK Parliament

That chart shows that inflation has been rising again in 2025, and it currently stands at 3.6% . According to the BBC, the International Monetary Fund (IMF) predicts that the UK will face the highest rate of inflation among G7 nations in 2025 and 2026.

However, don’t despair. There are steps you can take to safeguard your business from high inflation and keep your financial plans on track.

Keep reading to learn more about “sticky” inflation and discover four practical tips for protecting your business from it.

How “sticky inflation” could affect your business

When prices remain persistently above the target rate – known as “sticky inflation” – your business may face:

- Supply shortages, resulting in higher costs

- Falling sales, as consumers have less money to spend

- Increased borrowing costs, due to higher interest rates

- Rising operational costs, including utilities, transport, and business rates

- Increased staff costs, as employees demand wages that keep pace with inflation

- Higher prices for stock and supplies due to an increase in the cost of raw materials.

These rising costs could squeeze profit margins and make your cash flow unpredictable. As such, pricing, planning, and forecasting may become challenging.

However, your business might benefit from high inflation, for example, if it can easily pass on price increases to customers or if it offers essential goods and services.

Staying agile is key – proactively adapting your business to the changing economic situation could help you minimise the impact of high inflation.

4 practical steps you can take to protect your business from high inflation

Here are a few tips you may wish to consider:

1. Analyse and reduce your expenses

Conduct a thorough review of your outgoings and identify any opportunities to reduce your business costs. This might include:

- Encouraging flexible and remote working to reduce travel and office costs

- Focusing your marketing budget on strategies that deliver a healthy ROI

- Cancelling or downgrading underused subscriptions and software

- Negotiating with suppliers to secure more favourable terms

- Reviewing staffing structures to ensure maximum efficiency

- Moving to smaller premises or subletting surplus space

- Paying down high-interest loans as a priority.

Ensure that you cut unnecessary costs and avoid false economies that could jeopardise business performance and growth. Letting your most expensive staff go or cutting all marketing spend might reduce your outgoings significantly, but without staff and marketing in place, your business is likely to struggle.

2. Invest in efficiency and productivity

Improving efficiency might help your business absorb the higher costs associated with sticky inflation. Even small changes could significantly reduce wasted time, resources, and costs.

Recent research by Mitie found that UK employers lose over £485 million each week because of time wasted due to workplace inefficiencies.

The study highlights how physical workplace factors, such as Wi-Fi connection and building maintenance, contribute to productivity levels. For example, surveyed employees estimated that they lose 68 minutes every week to unproductive tasks such as finding a suitable meeting room.

As such, optimising your workplace, for example, by removing clutter and improving the layout, could boost productivity. You might also want to consider:

- Automating repetitive tasks

- Upgrading your technology

- Training and upskilling staff

- Investing in employee wellbeing

- Reviewing key workflows and streamlining inefficient processes

- Improving communication to minimise delays and duplicate work.

3. Consider adapting your pricing strategy

You might be wary of increasing prices in case this alienates your customers and makes it harder to attract new ones.

However, during persistent periods of high inflation, it’s crucial to keep your pricing strategy under regular review. This could allow you to protect your business by adapting to changing economic conditions while also easing the impact on customers by increasing prices gradually, rather than in one big jump.

If you’re open and honest about any changes in pricing and the reasons for this, you might find that the reaction from customers and prospects is more favourable than you’d expect.

Moreover, investing time and money in cutting unnecessary costs and improving efficiency could mean you don’t need to raise prices too aggressively.

4. Seek professional financial advice

A financial planner can stress test your business finances to see how higher inflation might affect things such as your cash flow, profit margins, and pricing.

At Sovereign, we use advanced cashflow forecasting to help business owners visualise their finances in the short-, medium- and long-term across various “what if?” scenarios.

Once we’ve identified any potential problem areas, we’ll work with you to create a practical action plan for keeping your business on track.

Knowing your numbers, staying flexible, and being proactive could ensure that your business thrives, even during challenging economic times.

Get in touch

If you’d like to find out more about how we can help your business adapt and prosper during periods of high inflation, we’d love to hear from you.

To learn more, please email hello@sovereign-ifa.co.uk or call us on 01454 416653.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

The Financial Conduct Authority does not regulate cashflow planning.

Approved by Best Practice IFA Group Ltd on 9/12/25