Over the last few months it’s been hard to avoid negative headlines about the state of the UK economy. Soaring inflation, the cost of living crisis, energy bills, the mini-Budget, rising interest rates and a looming recession all paint a picture of a nation under pressure.

While news outlets often focus on the sensational headlines, the truth is that there are reasons to be cheerful about the economy – here are four.

1. The FTSE 100 has hit a record high

If your pensions or investments are in a diversified portfolio, the chances are that you hold investments in the UK’s top 100 companies.

So, while news bulletins warn of recession, the UK stock market has hit an all-time record high.

The blue-chip share index reached an intra-day high of 7,926 on 8 February 2023, having beaten its previous all-time closing high on 4 February. The previous record closing high was 7,877 in May 2018.

Of course, as you have previously read, the stock market is not the economy as much of the earnings of FTSE 100 companies are from overseas. The FTSE 250 has yet to reach its previous high, set in 2021, for example.

Hopes that central banks will not have to raise interest rates much further (see below), adding to increasing hopes that the UK will avoid a recession in 2023, have driven up share values.

So, if you’re invested in the FTSE 100, it’s likely to have been a positive start to 2023.

2. Interest rates are unlikely to rise much further

In their last meeting, the Bank of England (BoE) Monetary Policy Committee voted to raise interest rates for the tenth consecutive time, to 4%.

While this will push up the borrowing costs of anyone with a tracker- or variable-rate mortgage, the BoE has dropped its pledge to continue raising rates “forcefully” and said that it believed inflation had probably peaked.

The BBC reports that analysts believe rates will now peak at 4.5% – below the predictions in the aftermath of last autumn’s turmoil.

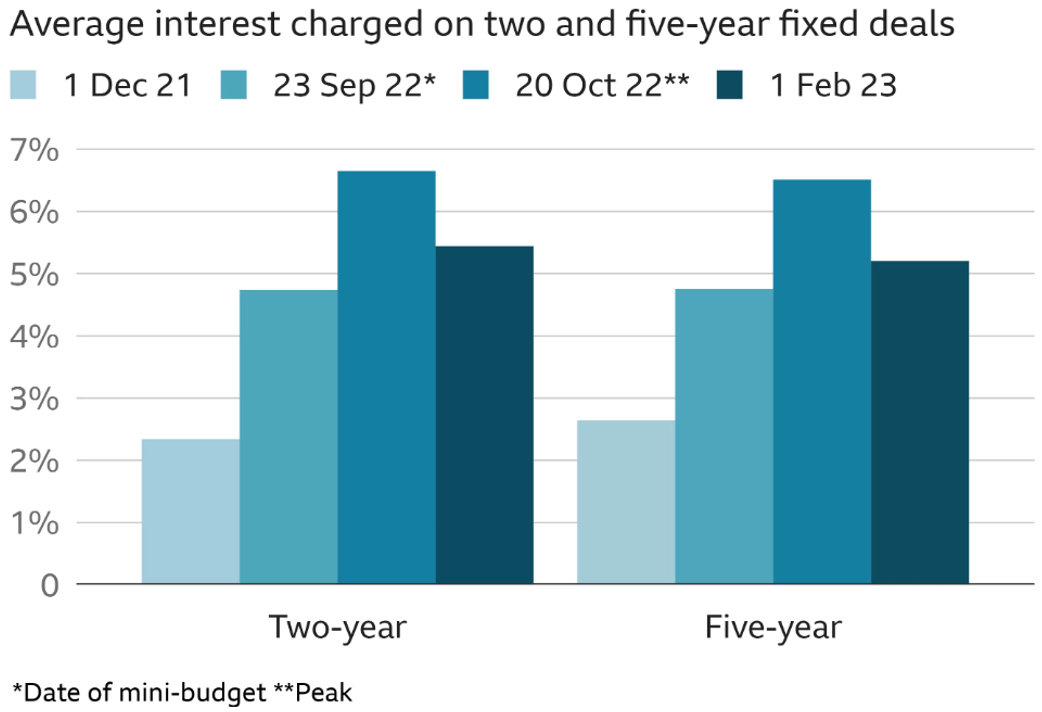

After the cost of new mortgages rose sharply after September’s “mini-Budget”, there are signs that the market is also stabilising.

As you can see from the chart below, the average cost of two- and five-year fixed-rate mortgages has fallen in recent weeks.

Source: BBC

If you are due to renegotiate your mortgage deal in 2023, you’re still likely to see a jump in your repayments, but perhaps not by as much as previously predicted. For example, the Guardian reports that HSBC have launched a five-year fixed-rate mortgage at 3.99%, much lower than the cost of deals available in late 2022.

3. Inflation has likely peaked

According to the latest Office for National Statistics (ONS) data, inflation stood at 10.1% in the year to January 2023. This is down 0.4% on December’s figure, and below October’s peak of 11.1%.”

The Guardian reports that the BoE expect inflation to fall rapidly in 2023, to 3.5% by the end of the year, and then to 1% in 2024.

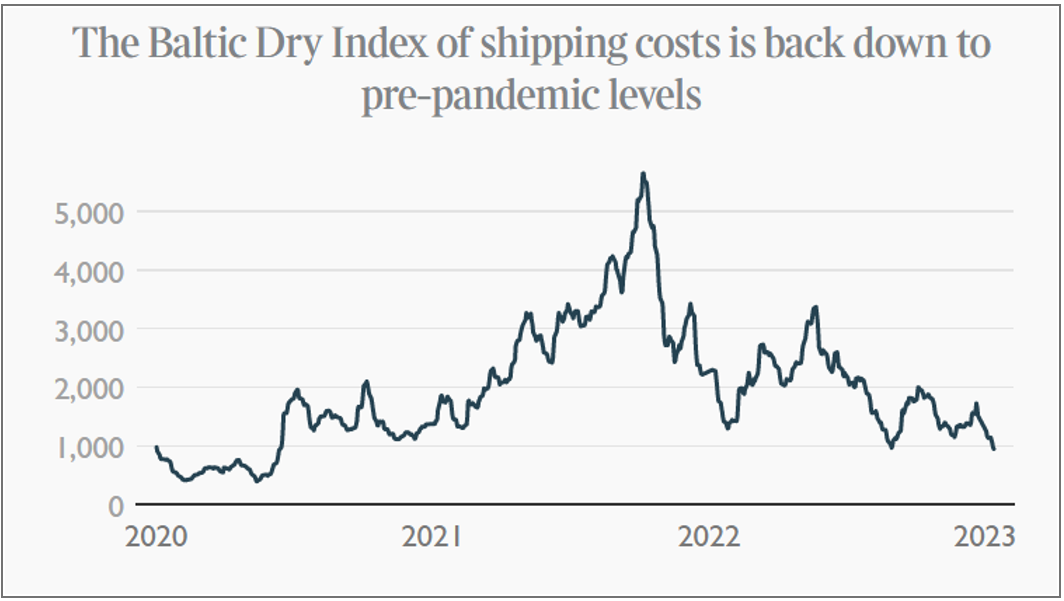

Here’s one example of why inflation will likely continue to fall.

One of the recent drivers of high inflation has been the huge rise in shipping costs as economies reopened, boosting demand for goods that the shipping industry could not meet.

In January 2023, freight rates were broadly back at their pre-pandemic levels. Data from maritime body Baltic Exchange showed the cost of container shipping had fallen nearly 90% from its highs in 2021.

Source: the Times

Lower inflation means the cost of goods and services are not rising as sharply, making your money go further.

4. Energy costs are falling

One of the other major contributing factors to soaring inflation has been the rise in the price of gas and oil as a result of sanctions imposed on Russia for its war in Ukraine.

The current Energy Price Guarantee (EPG) means that an average household with typical energy usage currently pays around £2,500 a year for their energy. This is set to rise to £3,000 in April 2023.

However, MoneyWeek reports that analysts expect energy prices to fall below the EPG from the summer.

Analysts at Cornwall Insight predict that the energy price cap will drop below the EPG rate from July to September 2023, estimating a new price cap of £2,361. They then predict the cap will be £2,389 between October and December.

Of course, this is still significantly higher than the price cap before the war in Ukraine. However, it does mean that your bills are likely to fall later this year, and that the government will no longer have to provide costly support to individuals and businesses.

Get in touch

If you want to make 2023 the year you take control of your finances, we can help.

To find out more, please get in touch. Email hello@sovereign-ifa.co.uk or call us on 01454 416653.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.