According to figures from JP Morgan, in 2018 the UK FTSE All-Share stock index fell by 9.5%.

If you’d had investments in the FTSE – and any well-diversified portfolio would – you might have experienced an immediate emotional reaction to that news.

You would naturally have been concerned about the value of your wealth, and perhaps you even considered whether you should be exiting the market before things got worse.

These types of emotional reactions, or behavioural biases, are perfectly normal. However, acting on them can affect your long-term security and cause you to make knee-jerk decisions that have significant consequences down the line.

Had you sold your FTSE shares at the end of 2018, for example, you’d have missed out on the 19.2% growth the index recorded the following year.

At times of uncertainty – such as during a pandemic with rampant inflation against the backdrop of a European ground war – it’s very easy for emotions to take over.

So, read on to discover three biases you might be experiencing right now, and how to ensure they don’t lead you to make the wrong decisions.

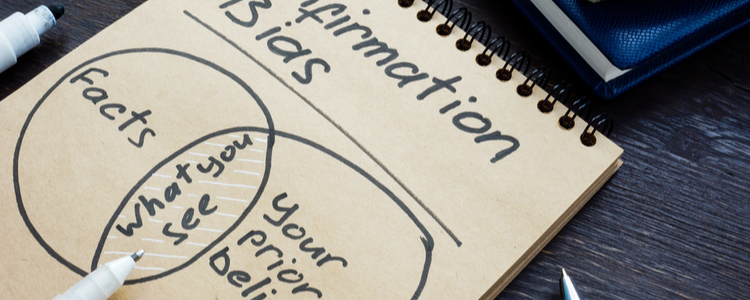

1. Confirmation bias

Arguably the most powerful of all behavioural biases, confirmation bias can affect any of your day-to-day decisions, and certainly when it comes to your finances.

When you start thinking about a financial decision that needs to be made, there’s a chance that you’ve already formed a preconceived idea.

For example, you may decide to research whether a specific type of investment would be right for you. However, in the back of your mind, you may have already decided it isn’t. So, you only search for information that confirms this belief while ignoring the evidence that could prove otherwise.

If you subconsciously believe “the stock market isn’t for you”, you’ll seek out information that confirms it’s a volatile place to invest. You’ll look for data that suggests you “lose money” as that will confirm what you already believe.

The effect of this bias is that you can fail to make the most of opportunities because you’re avoiding evidence that might make you question your beliefs.

2. Loss aversion

In 1979, Daniel Kahneman and Amos Tversky introduced the concept of “loss aversion”.

In simple terms, they showed that our natural desire is to prefer avoiding a loss to acquiring an equivalent gain. We feel losing £10 around twice as strongly as we would feel gaining £10.

When it comes to investing, loss aversion is a key behaviour in determining the level of risk you are willing to take with your investments.

If you feel loss aversion strongly, it could mean that you take on very little investment risk as you’re so concerned with the fear of “losing”.

Of course, taking on too little risk can also have a huge impact on your long-term plans.

Much of the growth in things like pension funds comes from stock market investments. So, investing too little could mean your fund doesn’t grow to the level you need it to in order to fund your desired retirement.

3. Herding bias

Herding bias is seen by many experts as one of the most dominant behavioural biases when it comes to investing.

Known in the modern world as “FOMO” (fear of missing out), it’s a behaviour where you convince yourself that a course of action is the right one simply because everybody else is doing it. In other words, it’s a tendency to mimic the crowd without considering your own judgement.

You can see a recent example of herding basis with the US retailer GameStop.

Historically, investors heavily “shorted” GameStop stock – essentially betting the stock price will fall. In early 2021, a group of investors who came together through social media channel Reddit began promoting GameStop stock. They took on huge hedge funds, who had shorted GameStop stock, forcing the funds to close their positions and lose billions of dollars.

Of course, the more people invested in this stock, the higher its price climbed.

The issue with GameStop is that its rampant share price didn’t match the company’s overall financial situation. In fact, the retailer was struggling and had plans to close 1,000 stores by the end of its financial year.

This artificially inflated share price means that a relatively small group of investors made large sums of money. However, many people jumped on the GameStop bandwagon and bought shares at inflated prices of more than $300.

When the share price tumbled – to just over $100 in February 2021 – many investors lost a significant amount simply because they had wanted to jump on a trend, whether or not it was the right thing to do in their individual circumstances.

The key thing to remember here is that your financial circumstances are unique to you. Your financial plan is also bespoke to you – so there should be no need to do what everyone else is doing. You just need to do what’s right for you.

Working with a financial planner can help you to manage your behavioural biases

One of the key benefits of working with a financial planner is that they can act as a sounding board to help you avoid making knee-jerk or emotional decisions that could damage your long-term plans.

Having another pair of eyes review the financial decisions you make can reduce the impact of your biases and ensure the decisions you make are right for you and your goals.

As a financial planner, we will work with you to create a long-term plan with your aspirations in mind. We will explain what your options are and the pros and cons of each, giving you confidence in the actions you take.

If you’re concerned about the current uncertainty, or you’d like to review your progress towards your goals, please get in touch. Email hello@sovereign-ifa.co.uk or call us on 01454 416653.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.