Over recent weeks, you will have seen the headlines that inflation in the UK has reached a 30-year high.

The BBC report that the cost of living rose by 5.5% in the year to January 2022. The Office for National Statistics (ONS) said that soaring food and energy bills are to blame, alongside increases in prices of furniture, food, and clothing.

With many analysts suggesting that the cost of living could rise even further in 2022, your clients may be justifiably concerned about the impact of inflation on their wealth. Here are three ways they could be affected.

1. Inflation can erode the value of cash savings

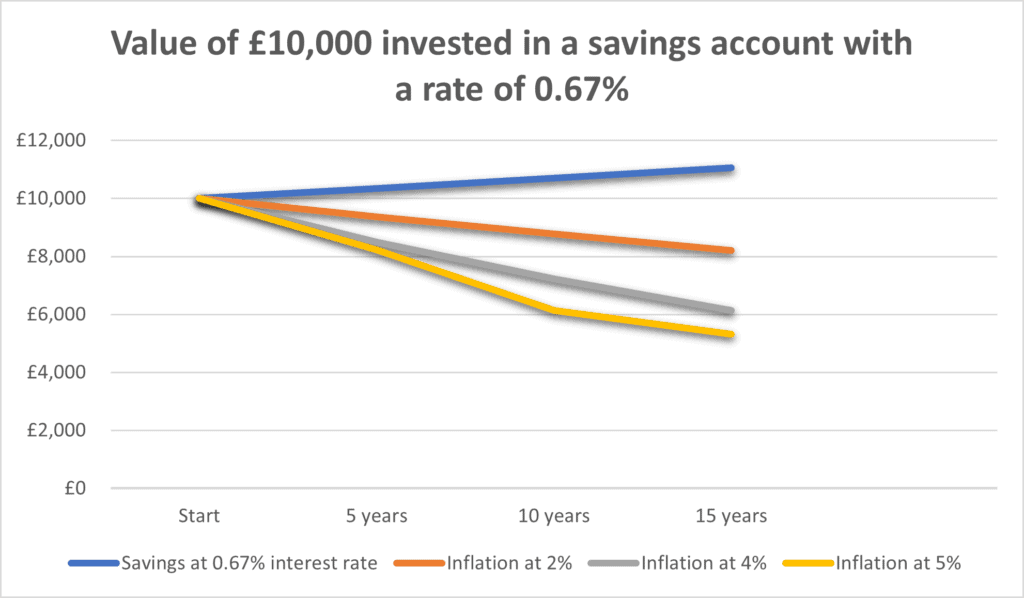

Recently, the insurer Royal London compared the growth of an average savings amount of £10,000 over 5, 10 and 15 years.

The figures show that the buying power of savings left in a high street savings account will decrease over time as inflation increases.

- If inflation rises to 4%, the purchasing power over 10 years will fall by more than a quarter (27%)

- If inflation remains at 5% over 10 years, clients would lose over a third (34%) of the “real value” of their money.

Even if the Bank of England were to keep inflation at their target rate of 2%, money in cash savings will be eroded over time, as the chart below shows.

Please note: Savings account interest rate taken from Times Money Mentor article with highest interest rate of 0.67% from Shawbrook Bank. This assumes no tax is paid on the interest. This assumes that inflation remains at 2%, 4% or 5% for the whole period.

Source: Royal London

What this chart shows is that, if clients leave a significant sum in cash savings, it is likely to lose value in real terms over time.

Investing money in assets such as bonds, shares, or funds can be one way of inflation-proofing wealth. Working with a financial planner can be beneficial here, as we can help a client to structure their investments according to factors such as their aims, time frame, and tolerance for risk.

Remember that the value of an investment can go down as well as up and a client may not get back the full amount they invested. Past performance is not a reliable indicator of future performance.

2. Inflation can mean clients end up being underinsured

Imagine a client took out a life insurance policy in 2002 for £150,000 and they died in 2022.

That £150,000 cover probably represented how much their loved ones would have needed to maintain their lifestyle at the time they took out the cover, considering their salary, outgoings, and the cost of goods and services.

However, on their death in 2022 a payout of £150,000 may be nowhere near enough for their loved ones’ needs at that time.

While the amount of protection a client wants may seem like a healthy sum today, 10, 15, or 20 years from now a client may well find that the lump sum their family receives may not be enough for their needs. If they have business protection this may also be the case.

It’s useful for a client to regularly review the amount of protection they have to make sure it has kept pace with the rising cost of living.

For any client wanting to take out protection now, adding an “indexation” option can help. This allows a policyholder to increase the amount that their plan covers each year in line with rises in the cost of living. The premiums will typically also rise by a small amount each year depending on the prevailing rate of inflation.

We can work with a client to ensure their existing protection remains appropriate. We can also arrange new index-linked cover to make sure their loved ones (and business, if applicable) are protected should the worst happen.

3. Inflation means clients have to think carefully about saving for retirement

It’s not uncommon for retirement to span several decades. So, when a client is working out how much is “enough” for their retirement, they need to carefully consider the impact of inflation.

The Bank of England’s inflation calculator demonstrates how inflation could reduce a client’s spending power in retirement.

Let’s say a client retired in 2010 and began taking an income of £28,000 to live comfortably. The average annual rate of inflation over the next decade was 2.9%. So, to achieve the same standard of living in 2021, a client’s income would have needed to increase to £38,201.16.

Now imagine the effect inflation could have over a full retirement that is likely to be two or three times longer, especially if the rate of inflation is much higher. If a client hadn’t planned for taking a greater income in their later years, they risk running out of money or they might have to pare back their plans.

Working with a financial planner can help a client to determine they have “enough” for their whole retirement – however long that lasts.

For example, we use sophisticated cashflow modelling to establish whether a client’s wealth will sustain them through retirement – even taking factors such as market volatility and inflation into account.

Get in touch

If you have clients who are worried about the effects of rising inflation, we can help. If you have clients that would benefit from advice, or you’re interested in how you can work more closely with us, please get in touch. Email hello@sovereign-ifa.co.uk or call 01454 416 653.