When preparing for retirement, pensions can be one of the most effective ways for your clients to build their wealth. A key reason for this is the generous tax relief individuals receive on their contributions.

As this relief is so valuable, there is an annual limit to how much a client can receive – the Annual Allowance.

In recent years, there has been a spike in the number of people who have breached this threshold. According to data from Money Marketing, the number of individuals who have exceeded the Annual Allowance has increased by 675% in the last five years.

If your clients want to enjoy a comfortable retirement, it’s important for them to build their wealth in a tax-efficient way. You’ve previously read about the importance of considering the Lifetime Allowance, so read on to find out why it’s so important for your clients to also pay attention to the Annual Allowance.

The government offers tax relief to encourage people to save for retirement

Each year, your clients can benefit from tax relief when they pay into their pension. The amount that they can receive is based on the level of tax they pay. For example, if your client is:

- A basic-rate taxpayer, they can receive 20% relief on their contributions

- A higher-rate taxpayer, they can receive 40% relief on their contributions

- An additional-rate taxpayer, they can receive 45% relief on their contributions.

As this benefit is so valuable, they have a limit on how much they can receive each tax year.

This allowance stands at £40,000 or 100% of your client’s annual earnings, whichever is lower. While your clients can continue to make contributions after they’ve exceeded the limit, they won’t be able to do so in a tax-efficient way unless they can make use of any “carry forward” from previous tax years.

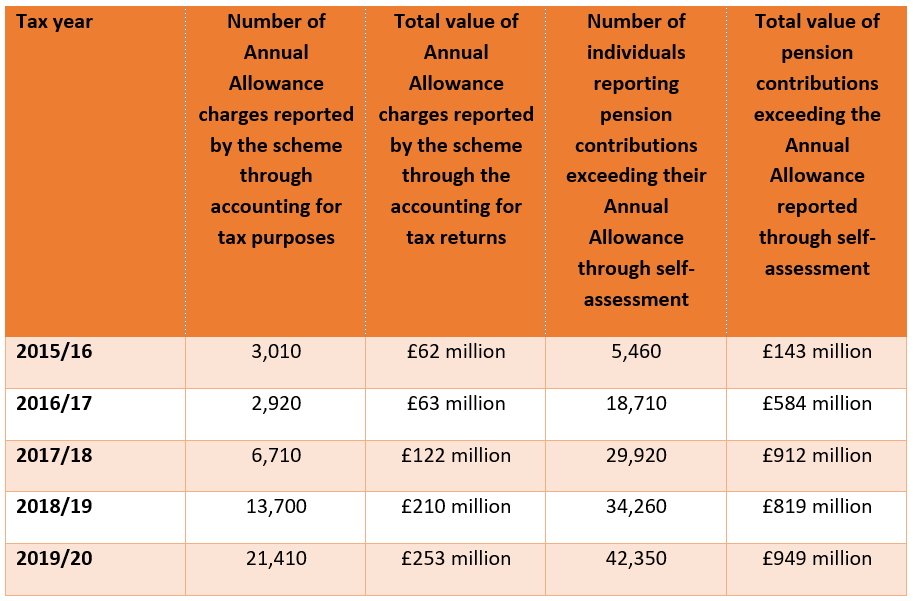

The number of individuals breaching the Annual Allowance is rising sharply

As you can see in the table below, there has been a surge in the number of people breaching the Annual Allowance in the past few years.

Source: Money Marketing

You can see from the table that the total tax charges individuals have paid for breaching the Annual Allowance has risen from £62 million in 2015/16 to £253 million in 2019/20.

Canada Life technical director Andrew Tully was quoted in Money Marketing as saying that one of the main reasons for this spike is the “complexity” of tax laws. Given how complicated the rules surrounding tax relief can be, it isn’t surprising that some Brits run into this issue.

Here are a couple of reasons why the complex rules can catch clients out.

If clients flexibly draw an income and continue to work, their Annual Allowance can fall

In recent years, there has been a shift towards more flexible retirements. According to a report published in Professional Adviser, two-thirds of people retiring in 2022 plan to continue working in some capacity.

While doing so can have variety of benefits, there are also tax implications to consider. One of the most important ones is that if your clients continue to work after drawing benefits from their pension, they could trigger the “Money Purchase Annual Allowance” (MPAA).

If they do, their Annual Allowance falls to just £4,000, which can make it much easier to breach the limit. This means that your clients will only be able to receive a much smaller amount of tax relief.

Furthermore, if your client earns more than £240,000 then they may be subject to the Tapered Annual Allowance.

Essentially, for every £2 their income goes over this threshold, your client’s Annual Allowance falls by £1. Clients earning over £312,000 will benefit from an Annual Allowance of just £4,000.

Finally, as we discussed in a previous article, clients also have a “Lifetime Allowance” for how much they can save into their pension in a tax-efficient way over the course of their lifetime. In the 2022/23 tax year, this stands at £1,073,100 and is frozen at this level until 2026.

Working with a financial planner can help your clients save in the most effective way

If your clients want to be able to build their retirement wealth in the most effective way, seeking professional advice can add real value.

Working with a financial planner can help them to navigate the potential tax pitfalls that they could encounter, reducing the chance of them breaching their allowances.

Seeking professional advice can also enable your clients to make informed decisions, so that they can grow their retirement wealth as effectively as possible. This can give them a greater sense of confidence that they’re on track to reach their long-term goals.

Get in touch

We’re here to advise you and your clients on all aspects of financial planning. If you have clients that would benefit from advice, or you’re interested in how you can work more closely with us, please get in touch. Email hello@sovereign-ifa.co.uk or call 01454 416653.

Please note

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.